Many Australians delay or avoid life insurance, often assuming it’s something to “sort out later.” But the real question is not just whether you need it, but what happens financially if it’s not in place.

1. Financial impact on your family

Life cover is primarily designed to provide a lump sum payment if you pass away or are diagnosed with a terminal illness. This payout can help your family manage immediate and ongoing financial obligations. Without it, your dependents may need to rely on savings, sell assets, or adjust their lifestyle significantly.

For example, policies generally aim to cover debts, replace lost income, and support future expenses such as education or daily living costs. Without this safety net, the financial responsibility shifts entirely to those left behind.

2. Debt and living cost pressure

Most households carry some level of debt—mortgages, personal loans, or credit cards. In the absence of life cover, these liabilities don’t disappear. They often become the responsibility of a surviving partner or the estate.

At the same time, regular expenses such as groceries, utilities, childcare, and rent continue. Life insurance, especially Income Protection, are specifically designed to help maintain cash flow during unexpected events, including illness or death.

Without insurance, families may be forced to make difficult financial decisions quickly, often during an already stressful time.

3. Emotional vs financial risk

While the emotional impact of losing a loved one is unavoidable, financial stress can make the situation significantly harder. Life cover does not remove emotional hardship—but it can reduce financial uncertainty.

Having structured cover in place allows families to focus on recovery and adjustment, rather than immediate financial survival. This distinction is often overlooked but becomes very clear in real-life situations.

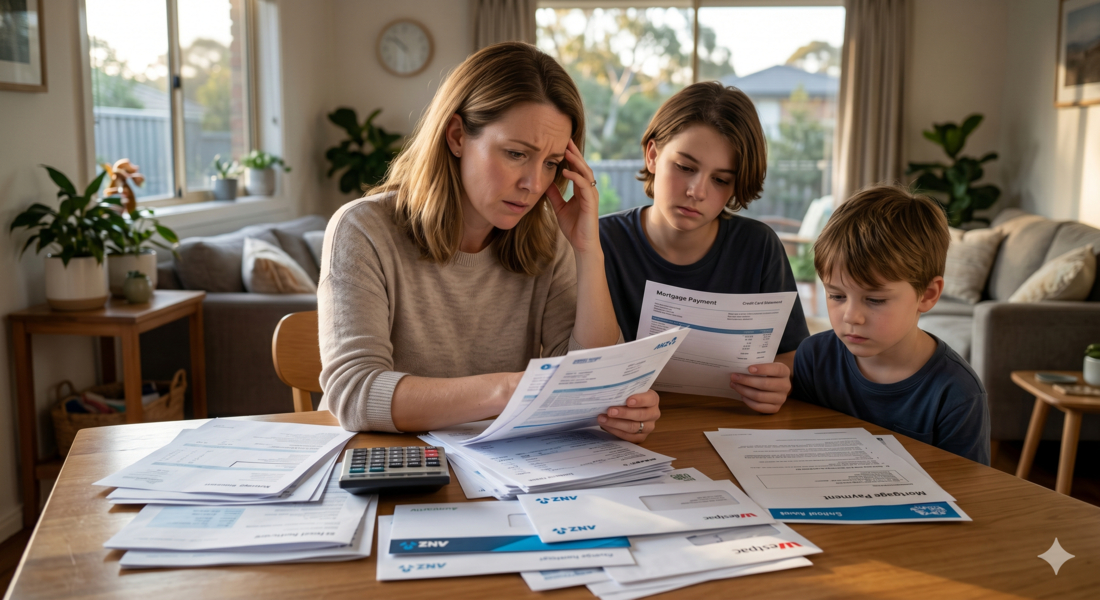

4. Realistic outcomes (no fear-mongering)

Not having life insurance does not always lead to financial hardship—but it increases the risk. Some individuals may have sufficient assets, minimal debt, or no dependents, making cover less critical.

However, for those with financial responsibilities, the absence of insurance typically means:

- Greater reliance on savings or family support

- Potential asset sales (including the family home)

- Reduced long-term financial stability

Life insurance products are structured to provide financial support during these exact scenarios, whether through lump sum benefits or income replacement.

Final Thought

Life insurance is less about preparing for the worst and more about protecting the people who rely on you. The real impact of not having it is rarely immediate—but it can shape your family’s financial future in ways that are hard to reverse.

If you’re unsure about your current cover”)—or any cover at all—consider booking a quick review with Flatmart. A simple conversation can understand general risks and available options.

Ready to get started?

Book a chat with a Finance & Mortgage Broker at Flatmart today.

General Advice Warning

The information provided in this article is of a general nature only and has been prepared without taking into account your individual objectives, financial situation, or needs. Before making any decisions, you should consider the appropriateness of the information and read the relevant Product Disclosure Statements (PDS).

Sources

- OnePath OneCare PDS — Zurich Australia Ltd (1 Oct 2024) — Income Secure Cover description pp.68–69

- AIA Priority Protection PDS — AIA Australia Ltd (15 Dec 2024) — Life Cover and benefit purpose overview pp.14–15

- Encompass Protection PDS — MLC Limited (16 May 2025) — Life Cover and Income Protection overview pp.6, 11

- TAL Accelerated Protection PDS — TAL Life Ltd (12 Dec 2024) — Life Insurance purpose and benefit structure pp.33–34