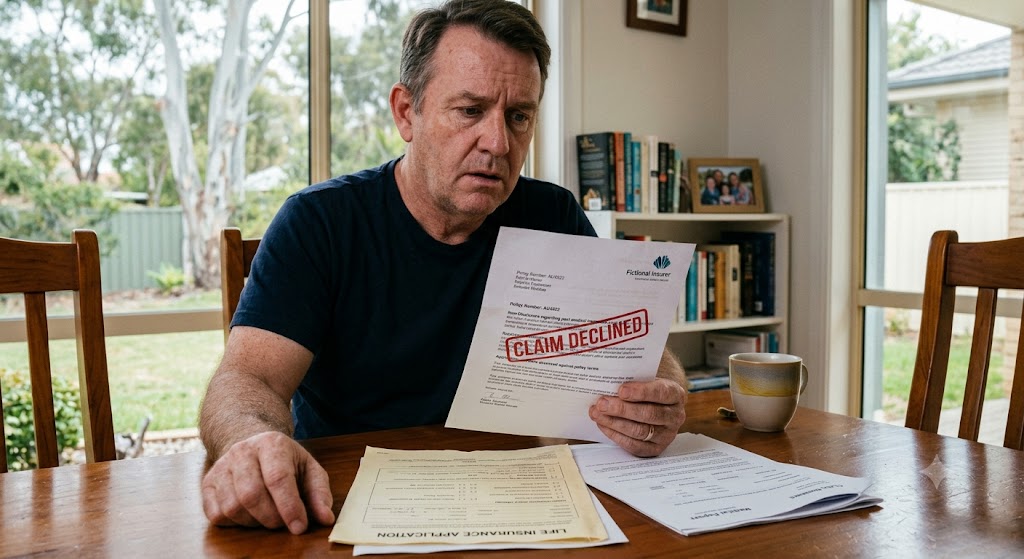

Life insurance is designed to provide financial support when a major event occurs, such as death, terminal illness, total and permanent disability, trauma, or inability to work due to illness or injury. However, a claim is not automatically paid simply because a policy exists. Insurers assess claims against the policy terms, the information provided at application, and any exclusions or conditions that apply.

1. Non-disclosure or misrepresentation

One of the most common claim issues is incorrect, incomplete, or misleading information provided during the application process. This may include medical history, smoking status, occupation, income, past insurance applications, hazardous activities, or lifestyle details.

Australian life insurance applications generally require the applicant to take reasonable care not to make a misrepresentation. If important information was not disclosed, the insurer may investigate whether the policy would have been accepted on the same terms. Depending on the circumstances, the insurer may reduce a benefit, vary the policy terms, or in serious cases treat the cover as if it never existed.

A simple prevention step is to answer every question carefully and include information even if you are unsure whether it is relevant.

2. Incorrect policy structure

A claim may also become more complex where the policy structure does not match how the cover is expected to work. For example, insurance held inside superannuation is generally owned by the trustee, not directly by the insured person. This means benefits may be paid to the trustee first and released only if superannuation law and the fund rules allow it.

A linked or attached cover can also affect claim outcomes. If one benefit is paid, it may reduce another benefit linked to the same policy. This does not necessarily mean the claim is declined, but it can mean the payout is different from what the policyholder expected.

3. Policy exclusions and special conditions

Life insurance policies can include general exclusions, cover-specific exclusions, and special conditions applied after underwriting. For example, a policy may exclude a particular medical condition, hazardous activity, or certain events depending on the product and the underwriting decision.

It is important to read both the PDS and the policy schedule, because the schedule may show individual exclusions, loadings, ownership details, benefit amounts, and expiry dates.

4. Prevention tips

To reduce the risk of claim issues, keep your application answers accurate, review your policy schedule after issue, update your cover when major life changes occur, keep premiums paid, and understand whether your policy is held inside or outside superannuation.

Final Thoughts

A declined claim is often linked to information, structure, definitions, exclusions, or policy conditions. The best time to understand these details is before a claim happens. Flatmart can help you review general life insurance options and understand the key areas to check before choosing or maintaining cover.

Ready to get started?

Book a chat with a Finance & Mortgage Broker at Flatmart today.

Book a life insurance review with Flatmart to understand how your existing cover works and what documents or policy details may need attention.

General Advice Warning: The information provided in this article is of a general nature only and has been prepared without taking into account your individual objectives, financial situation, or needs. Before making any decisions, you should consider the appropriateness of the information and read the relevant Product Disclosure Statements (PDS).

Sources

- NEOS Protection PDS (6 Dec 2024) - Duty to take reasonable care, misrepresentation consequences, ownership and structure, exclusions and claims sections, pp.7–12, 15, 19, 25, 51, 60.

- Zurich Wealth Protection PDS (1 Oct 2024) - Policy ownership, superannuation restrictions, risks, duty to take reasonable care, exclusions and claims, pp.6–9, 29, 64–69, 88.

- ClearView ClearChoice Combined PDS (13 May 2024) - Duty not to make a misrepresentation, policy remedies, cover commencement and claim-relevant terms, pp.24–25, 29.

- OnePath OneCare PDS — Zurich Australia Ltd / OnePath Custodians (1 Oct 2024) Application process, disclosure duty, policy schedule, superannuation acknowledgements and claim implications, pp.9–12, 130.

- AIA Priority Protection PDS (15 Dec 2024) Duty to take reasonable care, claim investigation, pre-existing condition exclusion, superannuation structure, pp.4–6, 169.