Life insurance in Australia is often misunderstood, leading many people to delay or avoid getting cover altogether. The reality is that most concerns come from outdated or incorrect assumptions. Let’s unpack the most common myths.

“I’m too young.”

Many people believe life insurance is only necessary later in life. However, insurance is not about age—it’s about risk.

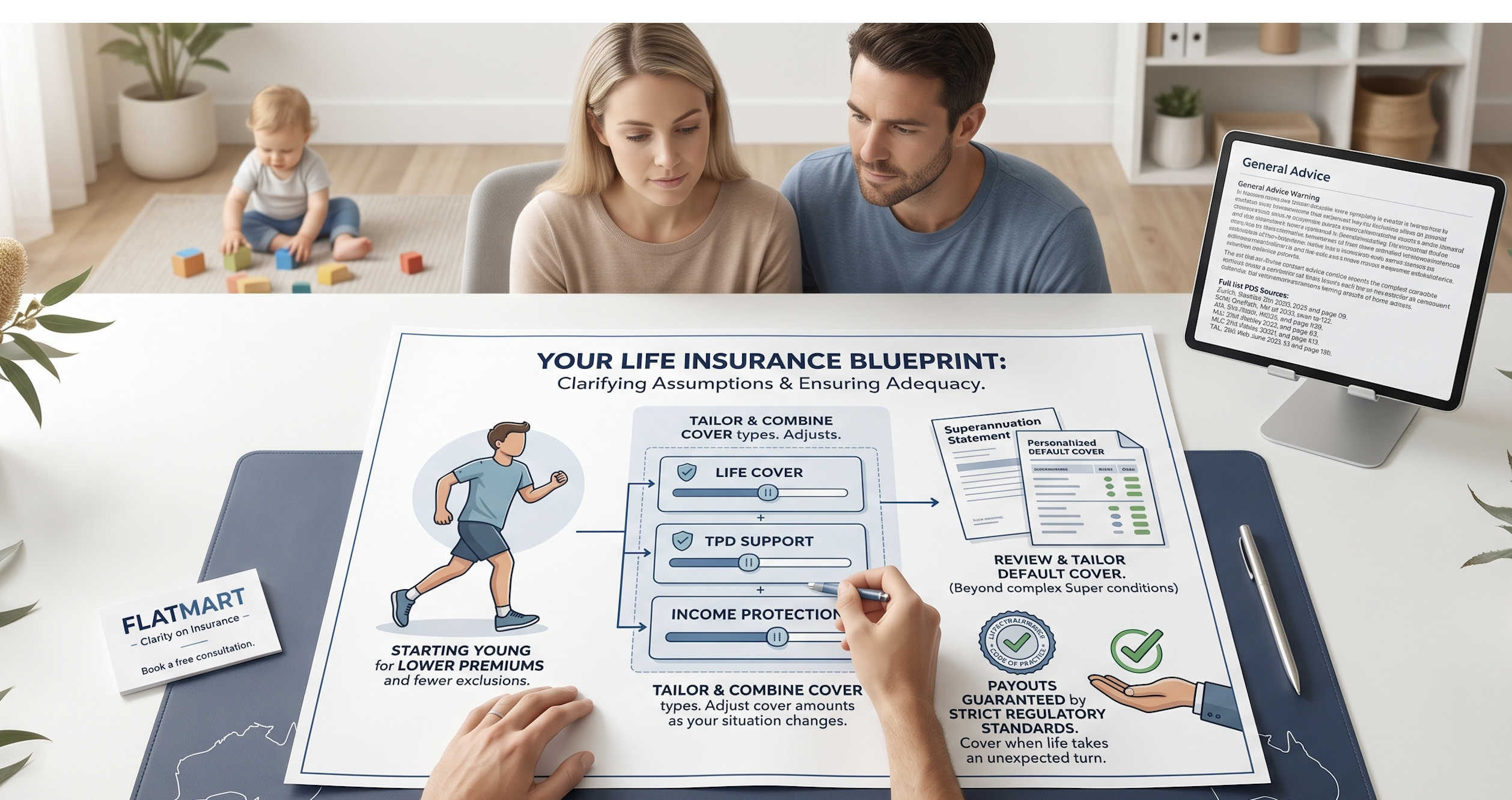

Income protection, for example, is designed to support you if illness or injury stops you from working by providing a monthly benefit to help cover living expenses. Starting younger can also mean lower premiums and fewer exclusions.

“Super is enough.”

While superannuation often includes default life insurance, it may not provide adequate protection.

Cover held through super is subject to release conditions under superannuation law, meaning benefits are paid to the trustee and only released when eligibility criteria are met. Default cover amounts are also typically not tailored to your personal financial situation.

“It never pays.”

A common myth is that insurers avoid paying claims. In reality, life insurance in Australia operates under strict regulatory standards, including the Life Insurance Code of Practice.

Policies clearly outline when benefits are paid:

- Life cover pays a lump sum on death or terminal illness

- TPD provides support if you cannot return to work

- Income protection offers ongoing monthly payments during disability

Claims are generally paid when policy definitions are met, and disclosures are accurate.

Clarifying the misconceptions

Modern life insurance is flexible and can be adapted to your needs. You can:

- Combine life, TPD, and income protection cover

- Structure policies inside or outside the super

- Adjust cover amounts as your financial situation changes

The real risk is not having enough cover when life takes an unexpected turn.

Final Thoughts

Believing common myths can delay proper protection. Life insurance helps safeguard your income and your family’s financial position by preparing for unexpected or adverse events.

If you’re unsure about your current cover, or haven’t looked at it in a while, reviewing your options can help you better understand what’s available.

Ready to get started?

Book a chat with a Finance & Mortgage Broker at Flatmart today.

Book a free consultation with Flatmart to gain clarity on how life insurance works and the options available.

General Advice Warning: The information provided in this article is of a general nature only and has been prepared without taking into account your individual objectives, financial situation, or needs. Before making any decisions, you should consider the appropriateness of the information and read the relevant Product Disclosure Statements (PDS).

Sources

- Zurich Wealth Protection PDS — Zurich Australia Limited (1 Oct 2024) — Policy overview and benefit structure pp.5, 32–40

- OneCare PDS — OnePath Life (Zurich Australia Limited) (1 Oct 2024) — Income Secure Cover (income replacement up to 70%) p.68

- AIA Priority Protection PDS — AIA Australia Limited (15 Dec 2024) — Income Protection and benefit descriptions pp.48–52

- Encompass Protection PDS — MLC Limited (16 May 2025) — Income Protection overview and policy structure pp.37–41

- TAL Accelerated Protection PDS — TAL Life Limited (12 Dec 2024) — Life, TPD, and Income Protection benefits overview pp.33–53