One of the most common questions people ask is whether life insurance is “locked in” once it starts. The short answer is no—most policies in Australia are designed to be flexible. However, how and when you make changes can have long-term consequences.

Policy Flexibility: More Than You Think

Most modern life insurance policies allow you to adjust your cover as your life changes. This could include updating your sum insured, changing premium structures, or even restructuring how your policy is held (inside or outside super).

For example, insurers highlight that cover is designed to adapt over time, with features allowing adjustments as circumstances evolve.

You can also cancel your policy at any time. Many insurers even offer a cooling-off period (typically 30 days) where you can cancel and receive a full refund if no claim has been made.

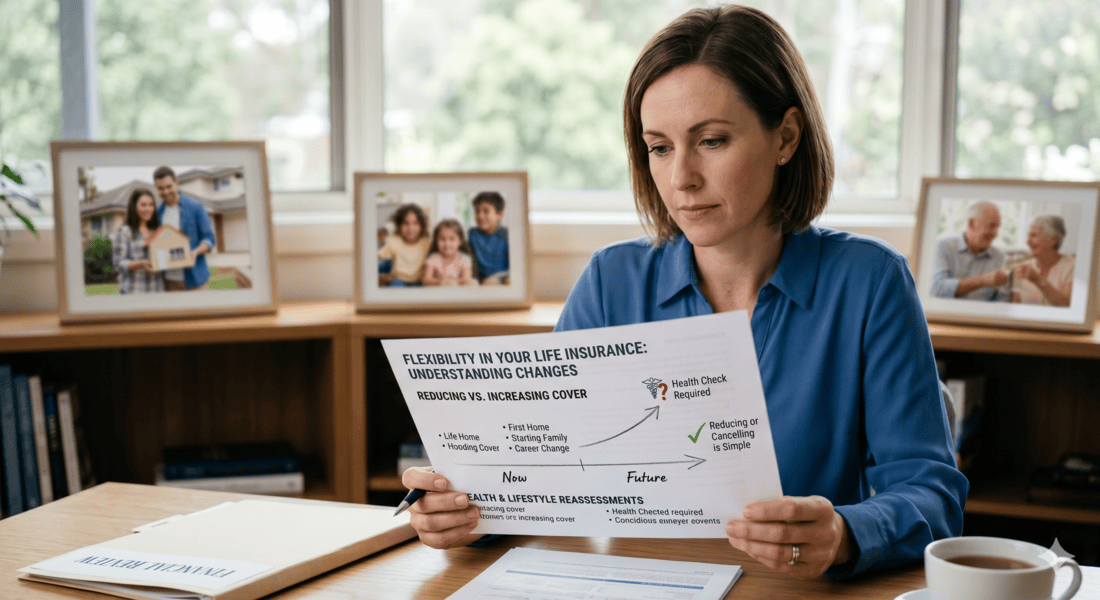

Increasing or Reducing Your Cover

Reducing cover is generally straightforward. If your financial obligations decrease—such as paying off a mortgage—you can lower your sum insured or cancel certain benefits.

Increasing cover, however, is different. In most cases, insurers will reassess your health, occupation, and lifestyle before approving higher cover. This process is known as underwriting.

Health Reassessment Risks

This is where many people get caught off guard.

When you first take out life insurance, your health status determines your terms. If you later develop a medical condition and then try to increase your cover, the insurer may:

- Apply exclusions

- Increase premiums

- Decline the increase altogether

Importantly, the duty to provide accurate information applies not just at the start, but also when making changes to your policy.

This means delaying cover decisions can limit your options later.

Thinking Long-Term Matters

Life insurance should not be treated as a short-term product. While flexibility exists, the best outcomes often come from setting up an appropriate structure early and reviewing it regularly.

Instead of relying on future changes, a more effective approach is to:

- Start with sufficient cover based on current and future needs

- Use built-in features (like indexation or future increase options)

- Review your policy as your life evolves

This helps reduce the need for re-underwriting later, especially when health may have changed.

Final Thought

Yes, you can change or cancel your life insurance—but not all changes are equal. Reducing or cancelling is simple. Increasing cover later can be more complex and dependent on your health at that time.

If you’re unsure about your current cover or any cover at all, consider booking a quick review with Flatmart. A simple conversation can understand general risks and available options.

Ready to get started?

Book a chat with a Finance & Mortgage Broker at Flatmart today.

General Advice Warning: The information provided in this article is of a general nature only and has been prepared without taking into account your individual objectives, financial situation, or needs. Before making any decisions, you should consider the appropriateness of the information and read the relevant Product Disclosure Statements (PDS).

Sources

a. OnePath OneCare PDS — Zurich Australia Ltd (1 Oct 2024) — Policy flexibility, changes and definitions pp.11, 55–56b. AIA Priority Protection PDS — AIA Australia Ltd (15 Dec 2024) — Cooling-off period and policy changes pp.6–7c. TAL Accelerated Protection PDS — TAL Life Ltd (12 Dec 2024) — Policy changes and underwriting obligations pp.5, 76